PPF vs VPF: Which is Better for Retirement Savings in India?

Investment options with fixed returns that are popular among conservative investors are the Public Provident Fund (PPF) and the Voluntary Provident Fund (VPF). They are both retirement plans with different eligibility, returns, and features.

PPF is open to all resident Indians and gives guaranteed returns with tax benefits. The lock-in period of 15 years attracts discipline, and, at maturity, both the interest income and maturity value are wholly exempt from taxation. For self-employed professionals, small entrepreneurs, or individuals not under the Employees' Provident Fund (EPF) system, PPF is one of the simplest retirement savings schemes.

VPF, which is an extension of the EPF scheme, is solely for salaried employees already covered under EPF. The tax treatment varies based on VPF withdrawal.

To read more about which is more suitable for you, keep on reading.

What Is PPF?

The Public Provident Fund (PPF) is a long-term, government-guaranteed savings plan. It aims to create a corpus at the time of retirement with assured returns. Anybody who is a resident Indian can open a PPF account. Guardians can open accounts on behalf of minors. There can be only one account per individual that can be opened through banks or post offices.

You have to deposit a minimum of INR 500 annually. The yearly limit is INR 1.5 lakh. Deposits can be in a lump sum or installments. The plan is for 15 years. You can withdraw the corpus or extend the account by 5-year chunks at maturity.

Interest rate tracks the government's quarterly review of small savings. PPF rate is 7.10% p.a., compounded, as of 2025. Interest is calculated on the lowest balance between the 5th of the month and the month-end. To earn maximum returns, invest before the 5th of the month.

PPF is tax-treated as EEE. Your contribution is eligible for deduction under Section 80C (up to the INR 1.5 lakh limit). Interest income and maturity proceeds are exempt from taxes. Even partial withdrawals and a loan facility are allowed with some limits after certain years.

PPF is apt for investors seeking capital protection, tax effectiveness, and a disciplined timeframe. Self-employed individuals, freelancers, and those not part of the formal EPF arrangement typically use it.

What Is VPF?

VPF refers to the Voluntary Provident Fund. It is an extension of the Employees' Provident Fund (EPF). Only EPF-covered salaried employees can avail themselves of VPF. The scheme provides for voluntary employee contributions over the mandatory EPF ratio.

The VPF contributions are deposited into your EPF account. The employers are not required to match the excess amount. While some employers still contribute only the statutory portion (12% of the basic pay), you can contribute up to 100% of basic pay plus dearness allowance, depending on your payroll configuration.

VPF derives the same rate of interest as EPF. For 2024–25, the government announced EPF interest as 8.25% p.a. The same rate applies to voluntary contributions that are credited to EPF/VPF.

Tax treatment is similar to EPF. VPF also typically comes under EEE: contributions (up to a limit), interest, and withdrawals are tax-free if conditions are fulfilled. Observe one vital exception. Interest on an employee's PF contributions above INR 2.5 lakh in a financial year can be taxed. High earners contributing should verify this ceiling and consult an expert tax advisor.

VPF is for salaried persons who seek greater fixed returns without forgoing tax advantage. It provides better returns than most small savings schemes. But it binds money to employment-based regulations and withdrawal terms.

Also Read: What Is City Compensatory Allowance: Are You Eligible?

PPF vs VPF: Key Differences

Both PPF and VPF are fixed-return saving schemes, but they function in significantly differing ways.

The following table contrasts their key features to guide investors to pick the one which is most appropriate for their investment needs.

| Feature | PPF (Public Provident Fund) | VPF (Voluntary Provident Fund) |

| Eligibility | Any resident Indian, including self-employed, salaried, or minors (through guardians). | Only salaried employees already enrolled in EPF. |

| Contribution Flexibility | Minimum INR 500 per year; maximum INR 1.5 lakh per year. Deposits can be made monthly or as a lump sum. | Employees can contribute any amount up to 100% of their basic salary + dearness allowance, over and above the statutory 12%. No fixed upper ceiling except salary. |

| Employer Involvement | No employer role. The entire contribution comes from the account holder. | Employers contribute only the statutory EPF share. No obligation to match voluntary contributions. |

| Tenure / Lock-in | Fixed 15 years; can be extended in 5-year blocks after maturity. | No fixed tenure. Remains active until retirement or job change. Withdrawals are allowed under specific conditions. |

| Interest Rate (2025) | 7.10% p.a., reviewed quarterly by the Ministry of Finance. | 8.25% p.a. (same as EPF), declared annually by EPFO. |

| Tax Treatment | EEE (Exempt-Exempt-Exempt): contribution (under Section 80C), interest, and maturity are all tax-free. | Generally EEE, but interest on employee contributions above INR 2.5 lakh in a year is taxable. |

| Accessibility | Universal, regardless of employment type. | Restricted to salaried employees with EPF accounts. |

Returns And Suitability of PPF and VPF

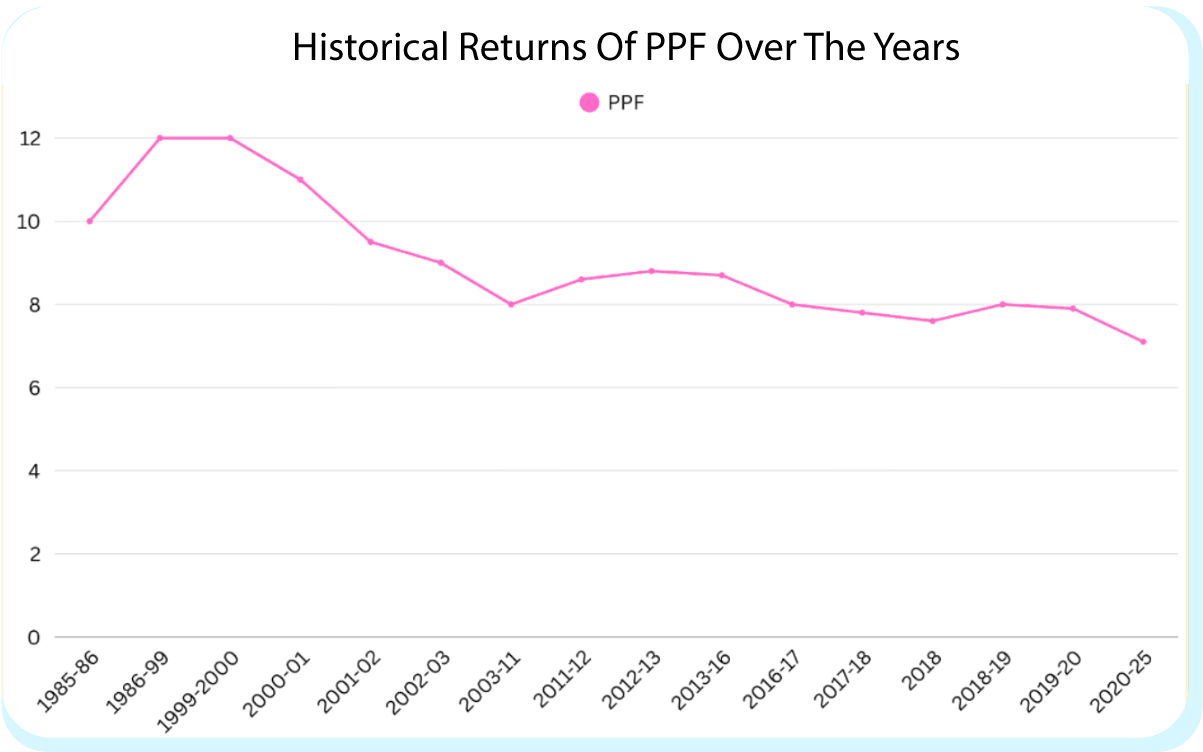

Historical PPF returns are given below:

| Financial Year | PPF Interest Rate (%) |

| 1985-86 | 10 |

| 1986-87 TO 1998-99 | 12 |

| 01.04.1999 TO 14.01.2000 | 12 |

| 15.01.2000 TO 28.02.2001 | 11 |

| 01.03.2001 TO 28.02.2002 | 9.5 |

| 01.03.2002 TO 28.02.2003 | 9 |

| 01.03.2003 TO 30.11.2011 | 8 |

| 01.12.2011 TO 31.03.2012 | 8.6 |

| 01.04.2012 TO 31.03.2013 | 8.8 |

| 01.04.2013 TO 31.03.2016 | 8.7 |

| 01.04.2016 TO 30.09.2016 | 8.1 |

| 01.10.2016 TO 31.03.2017 | 8 |

| 01.04.2017 TO 30.06.2017 | 7.9 |

| 01.07.2017 TO 31.12.2017 | 7.8 |

| 01.01.2018 TO 30.09.2018 | 7.6 |

| 01.10.2018 TO 31.06.2019 | 8 |

| 01.07.2019 TO 31.03.2020 | 7.9 |

| 01.04.2020 TO 30.09.2025 | 7.1 |

From the chart, you can see that PPF rates peaked during the 80s and have gradually declined after that. The modern rate (2024-25) is much lower, but still competitive for low-risk, tax-free savings.

Also Read: What Are VPF Tax Benefits?

Who Should Choose PPF?

PPF is better if you:

- Are in the informal sector, or in a freelance job, or self-employed, and do not have EPF coverage. PPF does not need an employer.

- Opt for fixed return, stable, tax-efficient long-term savings with a reliable government guarantee.

- Have a lock-in discipline preference. The rigid 15-year term imposes a savings discipline.

- Require flexibility of contribution timing (you can contribute a lump sum or in instalments) and desire tax-free interest and maturity.

Who Should Choose VPF?

VPF is a better option if you:

- Are you a salaried employee already covered under the EPF scheme. Only then can you avail VPF.

- Need more returns (since VPF interest = EPF interest, usually more than the existing PPF), and are willing to contribute a bigger percentage of salary.

- Manage less liquidity (since withdrawals are regulated under EPF/VPF terms and typically associated with retirement or resignation).

- Want to maximise retirement savings to take advantage of tax benefits, particularly if you're in a higher tax bracket.

Diversifying Beyond PPF/VPF

Diversification involves mixing savings options in a strategic manner. A combination of PPF, VPF, NPS, bonds, and SDIs provides stability, flexibility, and access to funds when required.

Why Consider Beyond PPF And VPF?

PPF and VPF are great for long-term wealth accumulation. However, both have limitations:

- PPF involves a mandatory 15-year lock-in.

- VPF involves tying funds to employment and typically until retirement.

To strike a balance between flexibility and safety, investors can include other fixed returns investments in India, including bonds and SDIs.

Flexibility and Tradability Through Bonds

Bonds can be used to supplement PPF and VPF with shorter tenures and better accessibility.

- Government securities (G-Secs): Supported by the RBI, accessible through the Retail Direct platform.

- Corporate bonds: High-grade variants offer regular returns with controllable risk.

- Tenure: These have a lower tenure, between a few months and 10 years, much lower than PPF.

- Liquidity: Can be sold in the secondary market, allowing investors to quickly sell it before maturity if money is required.

Platforms such as Grip Invest make it easier for retail investors to explore curated bonds with transparent access and improved liquidity.

Strategic Diversification

Mixing PPF/VPF with bonds and SDIs equals balancing long-term compounding and short-term liquidity. The following tips can be useful:

- Invest in PPF or VPF for retirement purposes with a tax advantage.

- Invest money in 3–5 year bonds or deposits where earlier access is required for goals.

- Invest a portion in liquid deposits to protect finances.

Conclusion

Choosing between the VPF and the PPF depends mainly on which is more suitable for your personal situation; no one is better than the other. Both are government-backed schemes with tax benefits, but they differ in structure and purpose.

The PPF provides a safe long-term savings avenue for a person without access to the EPF. The inherent discipline with the 15-year lock-in and tax-free returns makes it suitable for gradual wealth creation. PPF is favoured among self-employed professionals and conservative investors.

However, VPF works for an employee. It allows employees to further put in money over and above the mandatory EPF, with these contributions earning interest at the same attractive rate as EPF. For the year 2025, this is 8.25% per annum, a rate much beyond the 7.1% of PPF. Therefore, for someone looking to speedily grow a retirement corpus, VPF still remains a strong tool.

Most investors in practice use both. Keeping a part in PPF guarantees stability and tax-free savings in the long term, while adding additional contributions to the VPF allows a salaried person to optimise the returns.

For those looking to complement PPF and VPF with flexible, tradable fixed-income options, platforms like Grip Invest offer access to curated bonds and alternative investments that balance stability with liquidity.

FAQs On PPF vs VPF

1. Which is better: PPF or VPF?

Neither is absolutely good nor bad. PPF is good for those who don't have EPF. VPF is good for employees with salaried jobs covered under EPF, as it offers higher interest rates than PPF and makes it easy to invest with automatic payroll deductions.

2. Can I contribute to both?

Yes. If you are a salaried person covered under EPF, you can contribute to VPF and continue having a PPF account. That way, you can maximise tax savings and diversify retirement funds.

3. Is VPF taxable on withdrawal?

Taxation on VPF withdrawal depends on when you withdraw the funds. You can withdraw your VPF corpus in full after retirement or completion of 58 years of age. You may withdraw up to 75% before retirement for valid reasons like marriage, medical expenses, education, construction of a house, or at least one month of unemployment. Any withdrawal made before completing 5 years of opening the VPF account is taxable, and withdrawals made after 5 years are completely exempt from tax.

4. Can the self-employed invest in VPF?

No. VPF is applicable only to salaried employees enrolled under the EPF scheme. The VPF is not available to self-employed persons, but they can open a PPF account.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks, including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001